MMM: You Pulled Out Equity. Did You Accidentally Create Non-Deductible Debt?

With the self-employed tax filing deadline approaching, it's a good time to revisit one of the most common tax mistakes real estate investors make when refinancing their properties.

Many investors focus on finding the next deal, growing their portfolio, and accessing equity. But few pay enough attention to how those borrowed funds are handled after the refinance.

That oversight can have significant tax consequences.

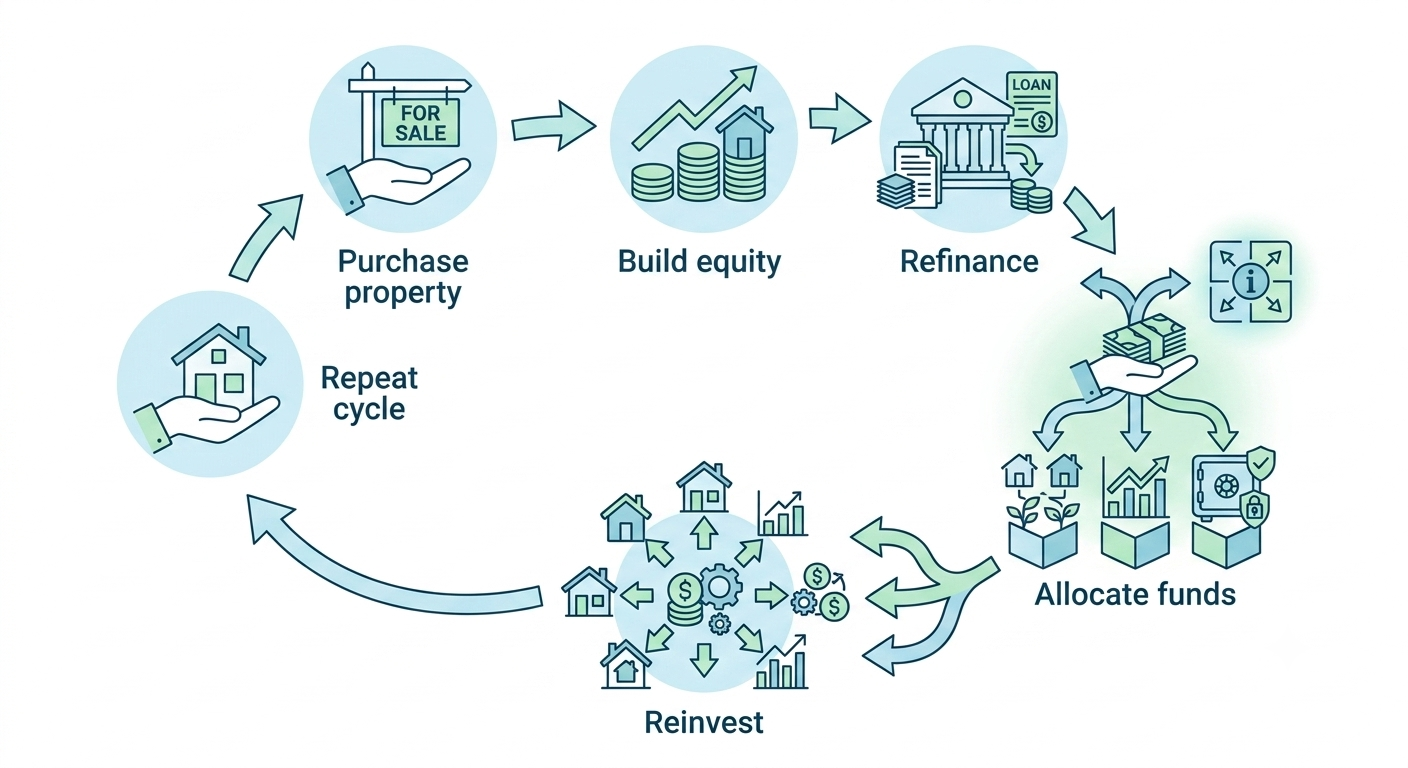

The Common Real Estate Investing Cycle

For many investors, the process looks something like this:

Purchase a property

Renovate it or hold it for appreciation

Build equity over time

Refinance the property

Pull out equity to fund the next investment

On the surface, this is a smart and common growth strategy.

The problem isn't the refinance itself.

The problem is what happens next.

What the CRA Actually Cares About

One of the biggest misconceptions among investors is that the deductibility of interest depends on which property the loan is attached to.

In reality, the CRA generally focuses on something much more important:

What was the borrowed money actually used for?

This distinction is critical.

The source of the loan matters less than the use of the funds.

If borrowed money is used for the purpose of earning income from a business or investment, the interest may be deductible. If the funds are used for personal purposes, the deductibility may be lost.

A Real-World Example

Let's say you refinance an investment property and pull out $200,000 in equity.

If that $200,000 is used directly to:

Purchase another investment property

Invest in income-producing assets

Fund a business investment

Acquire assets intended to generate income

there may be a strong argument that the interest on that borrowed money remains tax deductible.

However, many investors unintentionally create problems by changing the flow of funds.

How investors Accidentally Create a Tax Problem

A refinance is completed.

The funds are deposited into a personal chequing account.

The investor reimburses themselves for past expenses.

Some of the money goes toward:

Personal debt repayment

Household expenses

Vacations

Vehicle purchases

Other lifestyle spending

Then, with whatever remains, they invest.

This is where things become complicated.

Once borrowed funds become mixed with personal spending, it can become much more difficult to establish a clear connection between the loan and the income-producing investment.

In other words, the deductibility of the interest may be compromised.

Why the Flow of Funds Matters

Two investors can refinance the exact same property.

They can borrow the exact same amount.

They can have identical interest rates.

Yet one investor may end up with deductible interest while the other does not.

The difference often comes down to documentation, tracing, and the flow of funds.

Tax efficiency is frequently determined by structure, not just strategy.

Structure Matters More Than Most Investors Realize

Many investors spend considerable time analyzing market conditions, interest rates, and property values.

Far fewer spend time planning how refinanced funds will move from one account to another.

Yet that simple detail can have a significant impact on the long-term tax efficiency of a portfolio.

A well-structured refinance strategy can help preserve deductibility and maintain clear documentation.

A poorly structured one can create unnecessary complexity and potentially reduce tax benefits.

Final Thoughts

Refinancing can be a powerful tool for growing a real estate portfolio, but it's important to understand that accessing equity is only part of the equation.

How you handle those funds after the refinance can be just as important as the refinance itself.

If you're planning to pull equity from an investment property, reviewing the structure before moving the funds can help avoid costly mistakes down the road.