MMM: Where Does Your Next Dollar Go?

Most people believe they have an income problem.

But what if the real issue isn't how much money you make—it's how you organize it?

I recently came across a concept called the 5 Bucket System, and while the idea itself isn't revolutionary, the way it's structured really stood out. It's a simple framework that helps ensure every dollar you earn has a purpose.

If you're working toward financial freedom, investing in real estate, or building long-term wealth, this system is worth considering.

Every Dollar Needs a Job

Many people focus on earning more money, thinking that a higher income will automatically lead to wealth.

The truth is, income alone doesn't create wealth. Without a clear plan, even a high income can disappear just as quickly as it comes in.

I've experienced this firsthand.

Between running a mortgage business, managing a tax practice, investing in private businesses, owning rental properties, and juggling multiple financial responsibilities, money is constantly moving between accounts. Without a system in place, it can quickly become overwhelming.

That's exactly why the 5 Bucket System caught my attention.

What Is the 5 Bucket System?

The concept is straightforward: divide your money into five distinct categories, each with a specific purpose.

1. Bills

This bucket covers your essential monthly expenses, including:

Mortgage or rent

Utilities

Insurance

Groceries

Loan payments

Other recurring bills

By separating your fixed expenses, you always know your necessities are covered.

2. Emergency Fund

Life is unpredictable.

Unexpected repairs, medical expenses, or temporary income loss can happen at any time. An emergency fund provides financial security without forcing you into debt.

This bucket is designed to protect you when life doesn't go according to plan.

3. Investments

This is where long-term wealth begins.

Whether you're contributing to a TFSA, RRSP, FHSA, real estate investments, or a diversified investment portfolio, this bucket is dedicated to growing your wealth over time.

Consistent investing even in small amounts can make a significant difference over the long run.

4. Spending

Building wealth doesn't mean you can never enjoy your money.

This bucket is specifically for the things that make life enjoyable:

Dining out

Vacations

Entertainment

Hobbies

Shopping

Because you've planned for it, you can spend without guilt.

5. Opportunity Fund

This is my favorite bucket—and the one I believe many people overlook.

Instead of saving with no clear objective, this bucket is reserved for future opportunities that require quick action.

It could be used for:

A down payment on your next investment property

A renovation project

Starting a business

A private lending opportunity

Investing during a market correction

Any opportunity that requires immediate access to cash

The people who consistently seem to find incredible investment opportunities usually aren't just lucky.

They're prepared.

They've already built the financial flexibility to act when opportunity appears.

Cash Creates Options

One of my favorite sayings is:

Cash gives you options.

And options create wealth.

When you have available capital, you're able to make decisions others simply can't.

While others are trying to figure out how to finance an opportunity, you're already in a position to move.

That's often the difference between watching opportunities pass by and taking advantage of them.

Do You Need Five Bank Accounts?

Not necessarily.

Some people may prefer separate bank accounts, while others use budgeting software or multiple savings categories within a single account.

Personally, depending on your financial situation, you may even find yourself with more than five buckets.

The important lesson isn't the number of accounts.

It's making sure every dollar has a purpose before it reaches your everyday spending account.

Final Thoughts

Financial success isn't always about earning more.

Often, it's about creating a system that helps you make intentional decisions with the money you already have.

The 5 Bucket System provides a simple framework for organizing your finances, reducing stress, and preparing for both expected expenses and unexpected opportunities.

Because when opportunity knocks, the people with cash can act.

Everyone else watches.

MMM: The Bank of Canada Isn't the Only Institution Moving the Housing Market

When Canadians think about the housing market, one institution usually gets all the attention:

The Bank of Canada.

Every interest rate announcement sparks headlines, social media discussions, and countless predictions about where home prices and mortgage rates are headed next.

While the Bank of Canada plays a significant role, it's only one piece of a much larger puzzle.

Over the past two years, governments and regulators have repeatedly introduced changes that influence the housing market—often without changing interest rates at all.

The Institutions That Shape Canada's Housing Market

Many people assume interest rates are the biggest driver of housing activity. In reality, several organizations work together to influence how credit flows through the economy.

These include:

The Bank of Canada, which sets the overnight interest rate.

OSFI (Office of the Superintendent of Financial Institutions), which establishes lending rules for federally regulated banks.

CMHC (Canada Mortgage and Housing Corporation), which oversees mortgage insurance and qualification requirements.

Federal and provincial governments, which introduce financing programs, tax incentives, and housing policies.

Each of these institutions has the ability to affect borrowing costs, mortgage accessibility, and housing demand.

A Recent Example: OSFI's Domestic Stability Buffer

A great example happened just last week.

OSFI announced a reduction to the Domestic Stability Buffer (DSB)—the amount of capital Canada's largest banks are required to hold as a safeguard during periods of financial stress.

While this wasn't an official interest rate cut, some economists believe the move could have an economic impact similar to a 0.25% reduction in interest rates, giving banks more flexibility to lend and increasing the availability of credit.

I also created a short video explaining what this means and why it matters.

🎥 Watch the Instagram Reel here:

https://www.instagram.com/reel/DaD09HqTGXI/?utm_source=ig_web_copy_link&igsh=MzRlODBiNWFlZA==

The Bigger Picture

One message has become increasingly clear over the past two years:

Housing—and especially residential development—is simply too important to the Canadian economy to be left entirely to market forces.

When housing markets begin to slow, policymakers don't rely solely on interest rates to stimulate activity.

Instead, they often adjust:

Banking regulations

Mortgage qualification rules

Capital requirements

Government financing programs

Housing incentives

Tax policies

Each of these changes can influence lending, affordability, and overall market activity just as much as a change to the overnight rate.

Whether you see these actions as market stabilization or government intervention is ultimately a matter of perspective.

But one thing is certain: they shape the direction of Canada's housing market.

Don't Just Watch the Bank of Canada

If you're trying to understand where the housing market is headed, don't limit your attention to interest rate announcements.

Keep an eye on the entire system.

Changes from regulators like OSFI, updates from CMHC, and new government housing policies can all have meaningful impacts on buyers, homeowners, investors, and developers.

The more informed you are, the better equipped you'll be to make smart financial and real estate decisions.

Money Move of the Week

The biggest housing policy changes don't always come from interest rates.

Sometimes the most important developments happen quietly—without a single Bank of Canada announcement.

Understanding the broader system can give you an edge long before the headlines catch up.

MMM: Are We Heading Towards Stagflation?

Canada's inflation rate climbed to 3.2% in May, a figure that may not seem alarming at first glance. However, when combined with slowing economic growth and a gradually weakening job market, it raises an important question:

Could Canada be moving toward stagflation?

While we're not there yet, understanding the warning signs can help homeowners, investors, and everyday Canadians make smarter financial decisions.

What Is Stagflation?

Stagflation is a rare economic environment where inflation remains high while economic growth slows and unemployment rises.

It's particularly challenging because it impacts households from multiple directions:

Everyday expenses become more expensive.

Job security becomes less certain.

Interest rates may stay elevated longer than expected.

Unlike a typical economic slowdown, stagflation limits the ability of central banks to stimulate the economy without making inflation even worse.

Inflation Is Becoming More Widespread

One of the biggest contributors to May's inflation increase was gasoline, which rose 33% year over year. Overall energy prices increased 22%.

The impact of higher fuel costs doesn't stop at the gas station.

As transportation and operating costs rise, businesses often pass those expenses on to consumers, resulting in higher prices across the economy.

Recent data already reflects this trend:

Restaurant meals: +3.1%

Auto insurance: +6.2%

Rent: +3.5%

Perhaps even more important, inflation excluding gasoline also moved higher, suggesting that price pressures are spreading across multiple sectors rather than being driven by a single category.

Why This Matters

Inflation on its own is manageable. The greater concern is when inflation stays elevated while the broader economy continues to weaken.

This creates a difficult balancing act for policymakers.

Normally:

Rising inflation leads to higher interest rates.

Slowing economic growth leads to lower interest rates.

Stagflation presents both challenges simultaneously, leaving central banks with fewer effective policy options.

What It Means for Homeowners and Investors

If inflation remains persistent while economic conditions soften, Canadians could face several challenges:

Higher Borrowing Costs

Mortgage rates may stay elevated for longer, increasing borrowing costs for homebuyers and making refinancing less attractive.

Pressure on Consumer Spending

As households spend more on necessities like fuel, housing, and insurance, discretionary spending tends to decline, which can slow business growth.

Slower Housing Activity

Higher financing costs and reduced consumer confidence can put pressure on housing demand, leading to a more cautious real estate market.

Investment Volatility

Corporate profits may come under pressure as operating costs rise and consumer spending slows, creating a more uncertain environment for investors.

Are We in Stagflation Right Now?

Not necessarily.

A true stagflation environment would likely involve significantly higher inflation alongside a much weaker labour market than Canada is currently experiencing.

However, the recent data suggests that several key indicators are moving in a direction worth monitoring.

Rather than reacting to a single headline, it's important to watch the broader trends over time.

Key Indicators to Watch

Instead of focusing on daily news cycles, keep an eye on these economic signals:

Inflation: Is it continuing to rise across multiple categories?

Unemployment: Is the labour market weakening further?

Bond yields: Are investors expecting higher inflation and interest rates to persist?

Together, these indicators provide a clearer picture of where the economy may be heading than any single monthly report.

The Bottom Line

One inflation report doesn't define the future of the Canadian economy. But a consistent pattern of rising inflation, slowing growth, and weakening employment deserves attention.

Successful investing and long-term wealth building aren't about reacting to headlines—they're about recognizing trends early and making informed decisions.

For now, the focus remains on inflation, unemployment, and bond yields rather than short-term market noise. Staying informed and maintaining a long-term perspective will always be a stronger strategy than chasing the latest headline.

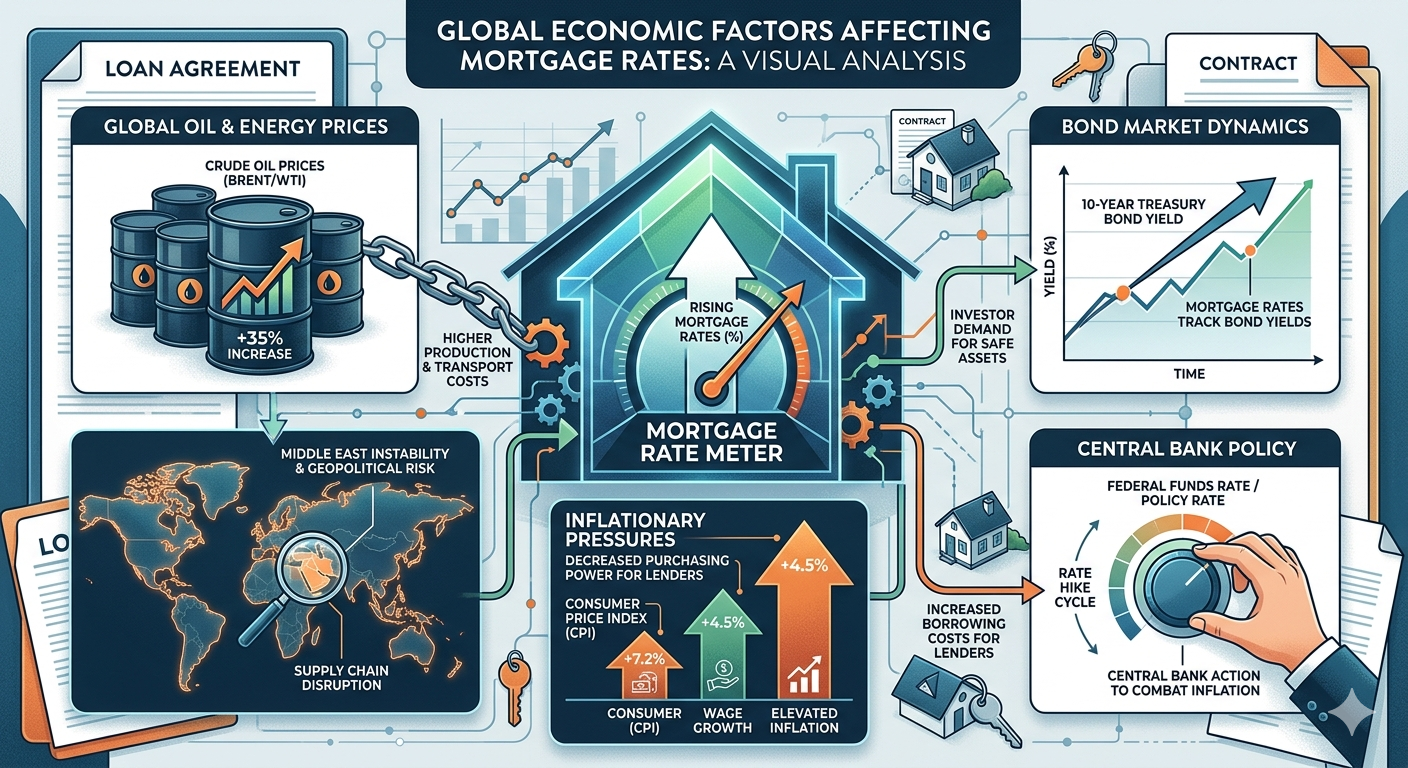

MMM : From Geopolitics to Your Mortgage Rate

The biggest global story right now is the tentative peace agreement between the United States and Iran.

After months of conflict, multiple countries have confirmed that both sides have agreed to a framework aimed at ending hostilities and reopening the Strait of Hormuz, with a formal signing expected later this week.

At first glance, this might feel like a distant geopolitical headline. But for Canadians watching mortgage rates and inflation, it actually matters a lot.

It all starts with oil

Following the announcement, oil prices dropped roughly 5% as markets began removing the “geopolitical risk premium” that had been built into energy prices.

That shift is important because oil has been one of the key drivers of inflation risk.

When oil prices rise, the impact doesn’t stay in one place. It spreads through the economy:

Transportation costs increase

Goods become more expensive to move and produce

Businesses pass those costs to consumers

Overall inflation rises

And when inflation rises, central banks are forced into a tighter position.

They either keep interest rates higher for longer, or increase rates further to bring inflation back under control.

For everyday Canadians, that shows up as higher borrowing costs, more expensive mortgages, and tighter monthly budgets.

The potential shift: easing inflation pressure

The positive angle here is that lower oil prices remove some of that inflation pressure.

As inflation concerns ease, bond investors typically become more comfortable accepting lower yields.

We’ve already seen the Canadian 5-year government bond briefly dip below 3% before bouncing back as markets digest the news and reassess whether the agreement will actually hold.

That matters because fixed mortgage rates are heavily influenced by the 5-year Government of Canada bond yield.

If bond yields trend lower over time, fixed mortgage rates tend to follow.

What the Bank of Canada is watching

In its most recent communications, the Bank of Canada highlighted two major risks:

Trade and tariff uncertainty

Oil-driven inflation

We still don’t have much clarity on tariffs.

But if this agreement is formally signed and holds, one of the major inflation risks facing the global economy may begin to fade.

That would be supportive for borrowers, supportive for fixed mortgage rates, and generally positive for investors who benefit from lower financing costs.

Not out of the woods yet

That said, markets are pricing in optimism right now but optimism is not the same as certainty.

The key moment to watch is the expected signing later this week, and more importantly, whether both sides actually follow through in the weeks that follow.

Until then, volatility is still very much on the table.

MMM: You Pulled Out Equity. Did You Accidentally Create Non-Deductible Debt?

With the self-employed tax filing deadline approaching, it's a good time to revisit one of the most common tax mistakes real estate investors make when refinancing their properties.

Many investors focus on finding the next deal, growing their portfolio, and accessing equity. But few pay enough attention to how those borrowed funds are handled after the refinance.

That oversight can have significant tax consequences.

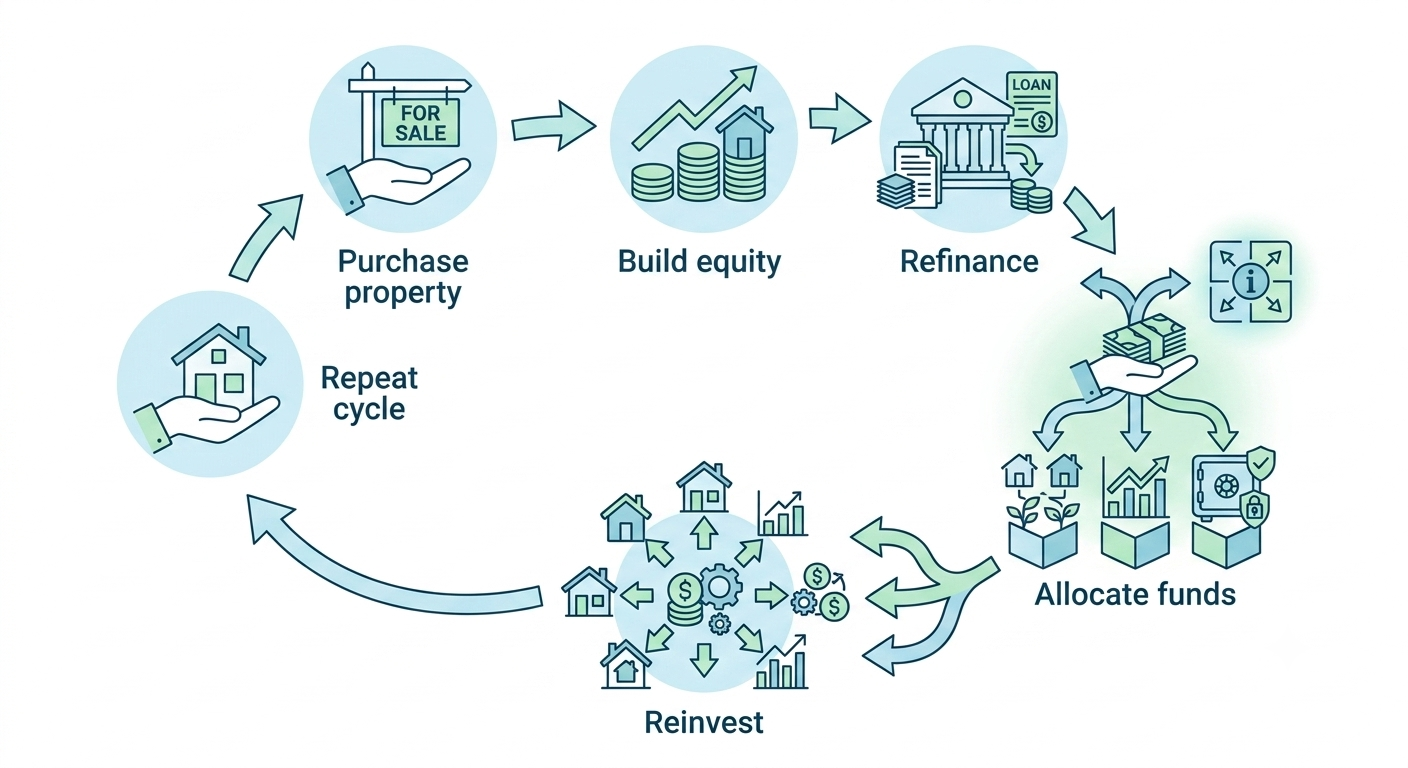

The Common Real Estate Investing Cycle

For many investors, the process looks something like this:

Purchase a property

Renovate it or hold it for appreciation

Build equity over time

Refinance the property

Pull out equity to fund the next investment

On the surface, this is a smart and common growth strategy.

The problem isn't the refinance itself.

The problem is what happens next.

What the CRA Actually Cares About

One of the biggest misconceptions among investors is that the deductibility of interest depends on which property the loan is attached to.

In reality, the CRA generally focuses on something much more important:

What was the borrowed money actually used for?

This distinction is critical.

The source of the loan matters less than the use of the funds.

If borrowed money is used for the purpose of earning income from a business or investment, the interest may be deductible. If the funds are used for personal purposes, the deductibility may be lost.

A Real-World Example

Let's say you refinance an investment property and pull out $200,000 in equity.

If that $200,000 is used directly to:

Purchase another investment property

Invest in income-producing assets

Fund a business investment

Acquire assets intended to generate income

there may be a strong argument that the interest on that borrowed money remains tax deductible.

However, many investors unintentionally create problems by changing the flow of funds.

How investors Accidentally Create a Tax Problem

A refinance is completed.

The funds are deposited into a personal chequing account.

The investor reimburses themselves for past expenses.

Some of the money goes toward:

Personal debt repayment

Household expenses

Vacations

Vehicle purchases

Other lifestyle spending

Then, with whatever remains, they invest.

This is where things become complicated.

Once borrowed funds become mixed with personal spending, it can become much more difficult to establish a clear connection between the loan and the income-producing investment.

In other words, the deductibility of the interest may be compromised.

Why the Flow of Funds Matters

Two investors can refinance the exact same property.

They can borrow the exact same amount.

They can have identical interest rates.

Yet one investor may end up with deductible interest while the other does not.

The difference often comes down to documentation, tracing, and the flow of funds.

Tax efficiency is frequently determined by structure, not just strategy.

Structure Matters More Than Most Investors Realize

Many investors spend considerable time analyzing market conditions, interest rates, and property values.

Far fewer spend time planning how refinanced funds will move from one account to another.

Yet that simple detail can have a significant impact on the long-term tax efficiency of a portfolio.

A well-structured refinance strategy can help preserve deductibility and maintain clear documentation.

A poorly structured one can create unnecessary complexity and potentially reduce tax benefits.

Final Thoughts

Refinancing can be a powerful tool for growing a real estate portfolio, but it's important to understand that accessing equity is only part of the equation.

How you handle those funds after the refinance can be just as important as the refinance itself.

If you're planning to pull equity from an investment property, reviewing the structure before moving the funds can help avoid costly mistakes down the road.

MMM: Canada Is Officially In A Recession. The Bigger Question Is: What Happens Next?

Canada officially entered what economists call a technical recession this week after recording two consecutive quarters of negative GDP growth.

Depending on your perspective, some people may view this as a major economic turning point, while others may argue the economy is still holding up reasonably well.

However, for those working in real estate, construction, development, mortgage financing, renovations, furniture sales, and home services, the news may feel more like a confirmation than a surprise.

Many are likely asking:

"Wait... we weren't already in one?"

Recessions Don't Always Start with GDP

Most people imagine a recession follows a straightforward sequence:

GDP falls

A recession begins

Jobs are lost

Housing weakens

In reality, economic slowdowns often develop gradually, with certain sectors feeling the impact long before GDP data officially confirms it.

In Canada's case, much of the housing and construction industry has been navigating these challenges for several years.

How the Slowdown Unfolded

1. Housing Demand Softened

As interest rates increased beginning in 2022, affordability worsened and buyer demand started to decline.

2. Transactions Slowed

Many buyers and sellers chose to wait on the sidelines, creating a significant drop in housing activity throughout 2023 and beyond.

3. Construction Activity Weakened

Developers faced higher financing costs, increased construction expenses, and greater uncertainty, causing many projects to be delayed or reconsidered.

4. Investment Began Drying Up

Pre-construction sales became more difficult, project viability declined, and some developments were postponed indefinitely.

5. Renovation Spending Declined

Homeowners became more cautious with discretionary spending, leading to slower demand for renovation projects and home improvements.

6. Suppliers Started Feeling the Pressure

Furniture retailers, appliance suppliers, building material companies, and manufacturers initially weathered the slowdown but increasingly faced challenges through 2024 and 2025.

7. Housing-Related Industries Slowed

Mortgage brokers, realtors, lawyers, appraisers, developers, contractors, and tradespeople experienced reduced activity as fewer transactions moved through the system.

8. Hiring Became More Cautious

Many businesses implemented hiring freezes, delayed expansion plans, and focused on controlling costs.

9. Unemployment Increased

As economic activity slowed, job losses and reduced hiring opportunities became more visible across multiple industries.

10. GDP Finally Confirmed the Slowdown

After years of weakening activity across key sectors, GDP data has now officially confirmed what many businesses and workers have already been experiencing.

Why This Recession Feels Different

One of the most interesting aspects of the current recession is how unevenly it is affecting Canadians.

For example:

A homeowner who locked in a low mortgage rate in 2021 may feel little financial stress.

A recent graduate struggling to secure interviews may view the economy very differently.

A developer attempting to launch a new condo project today may face significant challenges due to financing and market conditions.

This creates a situation where economic experiences vary dramatically depending on industry, location, and personal circumstances.

Can Government Policy Help?

The next major question is whether government initiatives can help slow or reverse the contraction.

One example is the recently announced GST/HST rebate programs aimed at encouraging housing construction.

If these incentives meaningfully improve project economics, they could:

Support new housing development

Create jobs

Increase construction activity

Improve investment confidence

Contribute to future economic growth

Whether these measures will be enough remains to be seen.

What Happens Next?

The key questions moving forward are:

How severe will this recession become?

How long will the slowdown last?

How broadly will it impact different sectors of the economy?

While the answers remain uncertain, one thing is clear:

Every recession eventually ends.

And every recession is followed by recovery.

The challenge for businesses, investors, and homeowners is positioning themselves to navigate the current environment while preparing for the opportunities that emerge when growth returns.

MMM: HELOC Strategy

I was supposed to be relaxing in Banff this weekend…

But instead, I somehow ended up thinking about mortgage structures again.

And I came across something that made me pause for a second.

Honestly, I’m hoping someone reads this and tells me why it doesn’t work.

Because if it actually does, there are likely a lot of investors and homeowners currently under cash flow pressure who could benefit from understanding it.

The Idea: Restructuring at Renewal

At renewal, most people simply sign into another standard amortizing mortgage.

But in some cases, there may be an opportunity to restructure a large portion of the balance into an interest-only HELOC instead.

Let’s break it down.

Example Scenario

Mortgage balance: $750,000

Home value: $937,500

Remaining amortization: 25 years

Renewal rate: 4%

Standard renewal payment:

≈ $3,958/month

The Alternative Structure (Hypothetical)

Federally regulated lenders may allow:

Up to 65% of property value as HELOC financing

Combined lending up to 80% loan-to-value

So in this example:

~$609,000 moved into an interest-only HELOC

~$141,000 remains as a traditional amortizing mortgage

The Result

New estimated monthly payment:

≈ $3,256/month

That’s roughly a 17% reduction in monthly payments

— without extending the amortization period.

Important Reality Check

This is where it gets interesting… but also where caution matters:

This can increase long-term interest costs

It is not suitable for everyone

Qualification and lender approval still apply

Structure depends heavily on individual risk profile and equity position

Why This Matters

For someone dealing with:

temporary cash flow pressure

rental property strain

or trying to redirect capital elsewhere

This kind of restructuring could potentially create breathing room without forcing a sale of assets.

Final Thought

I honestly think this is just the surface of what’s possible when it comes to creative mortgage structuring in Canada.

But I could be wrong.

So I’ll ask you directly:

If you think this strategy is flawed, reply and tell me why.

And if you know someone stuck in a cash flow squeeze, feel free to forward this to them.

MMM: The strategy that sits between debt reduction and investing

Most homeowners focus on one thing when it comes to their mortgage: paying it off as quickly as possible.

But many investors take a different approach.

Instead of simply paying down their mortgage, they use a strategy designed to gradually convert non-deductible mortgage debt into potentially tax-deductible investment debt — while building an investment portfolio in the background.

When structured properly, this strategy can create significant long-term financial benefits.

How the Strategy Works

In simple terms, here’s what happens:

Your mortgage principal gets paid down over time

As principal decreases, borrowing room opens up on a secured line of credit

That borrowed money is then invested into income-producing assets

The interest on the investment loan may become tax deductible

This allows homeowners to slowly shift debt from “bad debt” (non-deductible mortgage debt) into potentially more efficient investment debt while simultaneously growing investments.

Even the most basic version of this strategy can create meaningful long-term differences.

A Simple Example

On a $400,000 mortgage, a properly structured strategy could potentially result in:

Approximately $87,000 in estimated cumulative tax relief

Paying off the mortgage more than 3 years sooner

Potential long-term net worth improvement of approximately $466,000

The numbers can vary depending on interest rates, tax brackets, investment performance, and overall structure — but the long-term impact can be substantial.

The Important Part Most People Miss

The strategy itself isn’t usually the complicated part.

Implementation is.

This is where many people run into problems.

Proper setup, loan structure, account separation, tracing of funds, and tax documentation all matter. If these pieces are not handled correctly, the strategy may not work as intended from either a lending or tax perspective.

That’s why these conversations should involve both mortgage and tax planning considerations.

Structure First. Execution Second.

As both a mortgage broker and a CA, CPA, I approach these strategies from both the lending side and the tax side because the details matter.

Before implementing anything, it’s important to ensure:

The mortgage structure supports the strategy

Borrowed funds are properly traced

Investments qualify appropriately

Documentation is maintained correctly

The overall strategy aligns with long-term financial goals

When done properly, this can become a powerful long-term wealth-building strategy — not just a mortgage strategy.

Final Thoughts

Many homeowners only see their mortgage as debt.

Sophisticated investors often see it as a financial tool that can potentially help create long-term wealth when structured correctly.

The key is not just knowing the strategy exists — it’s understanding how to implement it properly.

Structure first. Execution second.

MMM: The Part That Worries Me Isn’t Rates

People keep comparing today’s housing market to either the 2020 COVID era or the 2017 mortgage stress test period.

But this cycle doesn’t really behave like either one.

And if you own real estate, have a mortgage, invest, or rely on employment income, that matters.

Canada recently lost 112,000 jobs over the last four months — the weakest stretch since the COVID shutdown era. Unemployment has climbed to 6.9%, youth unemployment is above 14%, population growth is slowing, and global uncertainty seems to increase every week.

At the same time, we still haven’t fully felt the long-term impact artificial intelligence could have on white-collar jobs over the next few years.

The issue today isn’t one single problem.

It’s multiple pressures stacking at the same time:

weaker hiring

slower population growth

high carrying costs

geopolitical instability

and lower consumer confidence overall

That combination changes behaviour.

Why This Market Feels Different

In 2020:

interest rates collapsed

governments injected stimulus

savings increased

and borrowing became extremely cheap

People felt relief quickly.

In 2017:

borrowing power was reduced

but employment remained relatively stable

and population growth stayed strong

Today feels different because there isn’t one clear pressure point.

Instead, it feels more like a slow grind:

higher costs

weaker confidence

slower economic growth

and increasing uncertainty around future employment

The Part Most People Underestimate

We haven’t really felt AI yet.

Most companies are still experimenting with it. But eventually, many business owners will ask the same question:

“Can software do this role cheaper?”

That doesn’t mean jobs disappear overnight. But it likely means:

leaner companies

fewer entry-level opportunities

and more pressure on certain types of income over time

Ironically, industries like trades, healthcare, infrastructure, and hands-on service businesses may become even more valuable moving forward.

So What Does This Mean for Real Estate?

I don’t necessarily believe this means a housing crash.

Canada still faces:

supply constraints

expensive construction costs

and high replacement costs

But I do think the strategy changes.

The “buy anything and wait” era may become weaker.

Going forward:

cash flow matters more

liquidity matters more

stable income matters more

and adaptability matters more

This may become a market where:

strong balance sheets outperform aggressive leverage

disciplined investors outperform emotional ones

and income growth matters more than appreciation alone

My Biggest Takeaway

The next few years will likely reward:

multiple income streams

low fixed expenses

liquidity

strong skills

and adaptability

Not fear.

Not panic.

Just discipline.

Because this market may not reward complacency the same way 2020 did.

But it could heavily reward people who stay flexible while everyone else freezes.

MMM- Housing Isn’t Driving the Economy Anymore

Over the past few years, I’ve been noticing a shift — a different kind of economy forming, at least within my network.

For a long time, housing did more than just provide shelter. Rising home values played a major role in supporting spending.

As home values increased, so did:

Access to credit

Willingness to take on risk

Overall consumer spending

But that dynamic is starting to weaken.

The Decline of Housing-Driven Liquidity

Home prices have come down from their peak, while borrowing costs remain elevated. The result is a noticeable compression in housing-driven liquidity:

Refinances are less beneficial

HELOC usage has become more cautious

Real estate transaction volumes are slower

This shift is significant because household consumption accounts for roughly 55–60% of Canada’s GDP.

Policy Is Responding — But Behavior Is Changing

We’re already seeing policy responses aimed at restoring activity:

Expanded insured mortgage programs

HST rebates

Zoning changes to increase housing density

However, when housing stops contributing to perceived wealth, consumer behavior changes.

Spending slows

Savings increase

Market turnover declines — in both real estate and small businesses

The Pressure Ahead: Mortgage Renewals

A large portion of borrowers renewing between 2025–2027 are expected to face payment increases of 20% or more.

This will further tighten household cash flow and reinforce more cautious financial behavior.

A Shift Toward Income and Cash Flow

What’s most interesting is how people are adapting.

There’s been a clear shift toward income generation:

More professionals are running businesses alongside full-time jobs

Growth in service-based businesses, especially tied to AI and automation

Increased interest in acquiring small businesses for cash flow

More Canadians are exploring opportunities outside the country for better returns

This shift is rational.

When asset appreciation becomes uncertain and leverage is more expensive, the focus moves toward controllable factors — income and cash flow.

What This Means for Real Estate Investors

This new environment changes how deals should be evaluated:

Cash flow and debt service coverage are now critical

Exit assumptions should be more conservative

Investment success depends less on appreciation and more on structure and income

A Healthier System — But a Different One

In many ways, this is a healthier system. But it requires a different mindset.

If you’re making decisions based on how the last cycle worked, you may be underestimating risk.

What Should You Do Next?

If you’re planning your next move — whether that’s:

Increasing income

Restructuring debt

Deploying capital

It’s worth taking a more strategic approach in today’s environment.

MMM: We just hit break even real estate - again.

A couple of years ago, detached pre-construction homes in my area were selling for around $1.4M.

We’re talking:

Double car garage

~2,400 sq ft

Standard family homes

A lot of people bought at those prices.

But as we moved through late 2025 into early 2026, something started to feel off.

A neighboring city — with better schools, more transit access, and stronger long-term development — was priced almost the same for resale homes.

That gap didn’t make sense.

And real estate doesn’t tolerate gaps for long.

The Quiet Shift

Fast forward to today…

Pre-construction pricing has quietly dropped to around $1.1M – $1.25M.

Resale prices have started following that trend.

Then came the real catalyst:

The HST rebate.

Effectively, that brought pricing down even further:

$1.1M → closer to ~$1.0M

That’s not a small adjustment — that’s a market reset.

It’s Already Showing Up in Resale

This past weekend alone, we saw:

$1.08M for a corner lot, 2,400 sq ft, with a finished rentable basement

$1.0M – $1.05M for similar homes without basements

This is the market adjusting in real time.

Why This Matters

Let’s break down that $1.08M deal:

If a buyer:

Puts 20% down

Rents out the basement

Their net housing cost drops to under $3,500/month.

That’s cheaper than renting just the upper portion of the same home.

Read that again.

We’re now at — or very close to — break-even real estate in parts of the GTA… assuming rents hold.

Two Things You Need to Understand Right Now

1. Markets Always Balance

Real estate behaves like a lake.

Throw a rock in, you get waves.

But eventually, everything settles.

Markets move together over time.

There are no permanent mismatches.

2. The HST Rebate Isn’t Just a “Buyer Perk”

It’s a pricing reset mechanism.

And it doesn’t stay contained to pre-construction.

It:

Pulls resale prices down

Resets buyer expectations

Creates appraisal risk for pre-construction closings over the next 1–2 years

The Bottom Line

We’re in the middle of a market rebalancing.

And these are the moments that matter most.

Because when pricing resets and opportunities open up…

The people who act make the biggest gains.

MMM: March was the warning. Renewals are next.

Inflation came in hotter than expected.

2.4% in March (up from 1.8%) — but that headline doesn’t tell the full story.

Gasoline prices alone are up:

+5.9% year over year

+21% month over month

A lot of the media is suggesting that the Bank of Canada is downplaying oil and choosing to “ignore” its impact.

I wouldn’t.

Because inflation doesn’t hit all at once — it moves in waves.

How Inflation Actually Spreads

Think of it in phases:

Phase 1: Energy spikes (we’re here)

Phase 2: Transportation and shipping costs rise

Phase 3: Wage pressure builds

Phase 4: Everything gets more expensive

Yes, it’s simplified—but directionally, this is how it plays out.

And once costs go up, they rarely come back down.

Why This Matters More Than You Think

2026 is shaping up to be a major mortgage renewal year.

A large number of Canadians locked in their mortgages during 2021.

Now, they’re approaching renewal…

In a completely different rate environment.

What’s Happening Right Now

Variable rates: Mostly unchanged

Fixed rates: Still elevated (bond yields are up ~0.4% from February lows)

Markets: Rate cuts are no longer being priced in, with about an 82% chance rates hold in April

The Real Problem

In a normal cycle, homeowners have options at renewal:

Refinance

Consolidate debt

Extend amortization

Access equity

But today?

Home prices in many markets are down 20–25% from their peak.

That limits flexibility.

You may want to restructure your mortgage—but it’s not always possible anymore.

What I’m Telling My Clients Right Now

1. Start Early — Earlier Than You Think

Don’t wait until 30, 60, or even 120 days before renewal.

Some of my clients start planning up to 11 months in advance—and they’re the most prepared.

2. Stop Chasing the “Best Rate”

You’ll hear this often, but it matters more now than ever:

It’s not just about the interest rate—it’s about cash flow.

3. Think Like an Investor

Your mortgage isn’t just a payment—it’s a tool.

Structure it so you can:

Adapt if rates change

Access equity when needed

Avoid getting stuck

Bottom Line

Inflation is picking up again.

Markets are reacting.

And mortgage renewals are heading straight into it.

March was the warning.

April will show if it’s real.

May might be too late.

MMM: Why self-employed people “pay less tax” (explained)

If you’re self-employed and have no idea why your accountant tells you to pay yourself a certain way…

Or you’ve heard that business owners “pay less tax” but don’t really understand how…

Let’s break it down with real numbers.

A Real Scenario

I recently worked through this with a client while filing their return.

Their corporation earned about $50,000 in net income in its first year.

They needed the cash, so leaving it in the corporation wasn’t an option.

So the question became:

How should you pay yourself?

Your Two Main Options

As a business owner, you typically have two ways to pay yourself:

Salary

Dividend

Same $50K.

Very different tax outcomes.

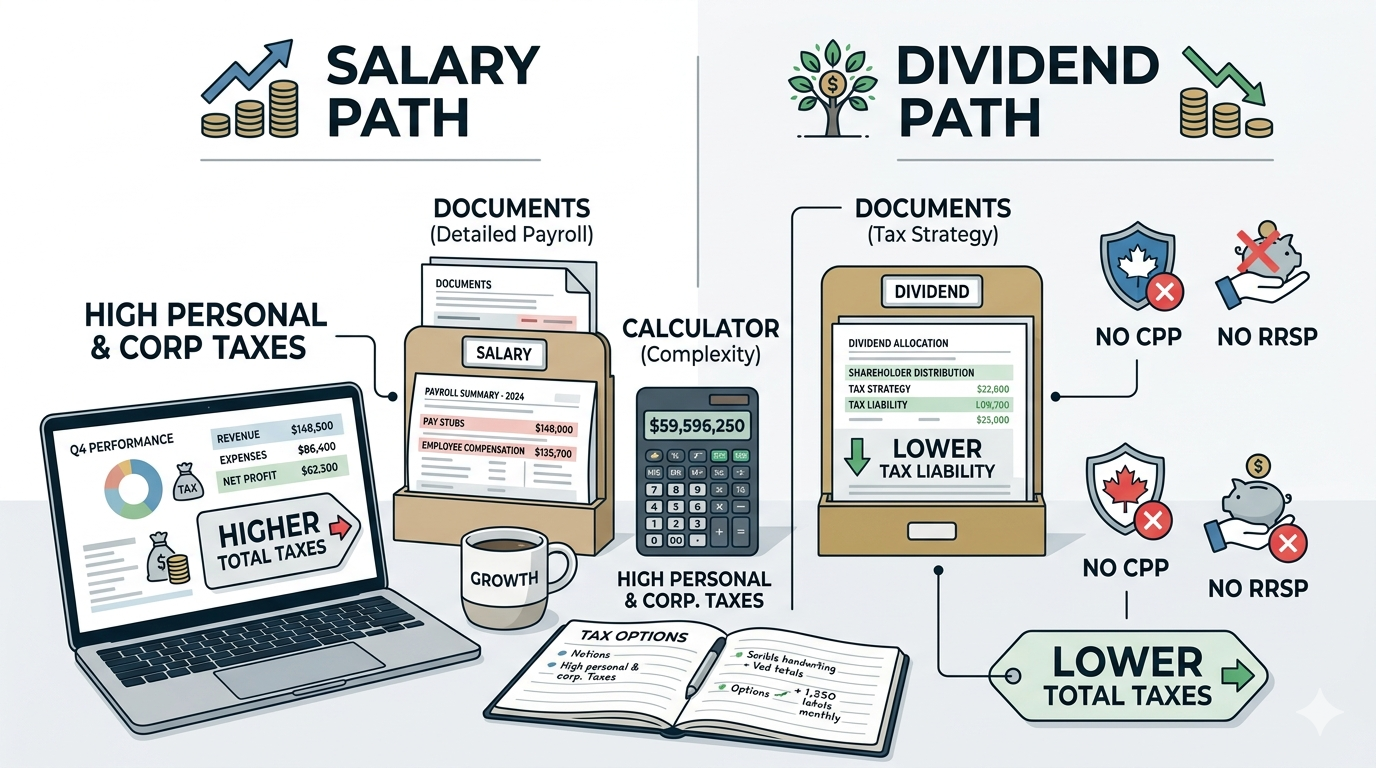

Option 1: Salary ($50K)

Here’s how it works:

The corporation pays you a $50,000 salary

Corporate income is reduced to $0 → no corporate tax

You pay personal tax + CPP (both employer and employee portions)

End Result:

Approximately $15,000 in total tax and CPP

Option 2: Dividend

This option involves a few more steps:

Step 1: Corporate Tax

$50,000 × 12.2% = ~$6,100

Remaining: $43,900

Step 2: Pay Dividend

You receive $43,900

Grossed up to about $50,500 taxable income

Step 3: Personal Tax

Federal tax: ~$6,800

Federal tax credit: -$4,300 → $2,500 net

Ontario tax: ~$2,200

Ontario tax credit: -$1,800 → $400 net

End Result:

$6,100 (corporate tax) + $2,900 (personal tax) = ~$9,000 total tax

The Trade-Off Most People Miss

At first glance, dividends look like the obvious winner.

You save about $4,000 in taxes

But here’s what often gets overlooked:

No CPP contributions

No RRSP contribution room

Many business owners don’t even realize they’re making this trade-off — it often gets defaulted during tax filing.

Why This Changes Over Time

The math isn’t static.

At different income levels, the strategy shifts.

Example at $100K income:

Dividends → ~$22,000 tax

Salary → ~$28,000 tax + CPP

You still save with dividends — but the gap narrows.

And at higher income levels, things like RRSP room and long-term planning become more important.

My Take

The goal isn’t just to pay less tax…

It’s to make better financial decisions over time.

How you pay yourself is one of the most important financial levers you have as a business owner.

Final Thoughts

There’s no one-size-fits-all answer.

The right strategy depends on:

Your income level

Your need for cash

Your long-term financial goals

If you’re self-employed and unsure what makes sense for your situation, it’s worth taking the time to get this right.

Because small decisions today can have a big impact over time.

MMM: Rates moved Most people missed it.

Over the past few weeks, I’ve been having the same conversation again and again:

“Should I take my lender’s renewal offer… or wait?”

If that’s something you’ve been wondering too, you’re not alone.

And if you’re still holding a rate from early March that hasn’t expired yet —

you may want to seriously consider taking it.

Let’s break down why.

Rates Have Already Moved

Fixed mortgage rates are closely tied to the Canada 5-year bond yield — and recently, that’s been on the rise.

Over just a few weeks:

The Canada 5-year bond yield jumped to around 3.08%

That’s an increase of about 0.45%

At one point, it even spiked close to 0.65%

When bond yields rise, fixed mortgage rates follow — often quickly.

What Caused the Shift?

Here’s the short version of what’s been happening globally:

Ongoing Middle East conflict pushed oil prices higher

Rising oil prices increased inflation risk

Higher inflation expectations caused bond yields to jump

Even the Bank of Canada has acknowledged:

More uncertainty

Higher inflation risk

Slower economic growth

Where People Get It Wrong

This is something I see every cycle:

When things feel calm → people lean toward variable rates

When things feel uncertain → people rush into fixed rates

The problem?

By the time it feels risky…

👉 Fixed rates have already gone up

👉 And you’re locking in too late

The best time to consider fixed rates is usually when no one is talking about them — not when everyone is reacting.

The Bottom Line

If your mortgage is renewing in the next 3 to 6 months, here’s what matters most:

Don’t overthink trying to “time” interest rates

Don’t ignore a solid offer that’s already in front of you

Focus on strategies that have a bigger impact, like:

Debt consolidation

Re-amortization

Setting up a HELOC

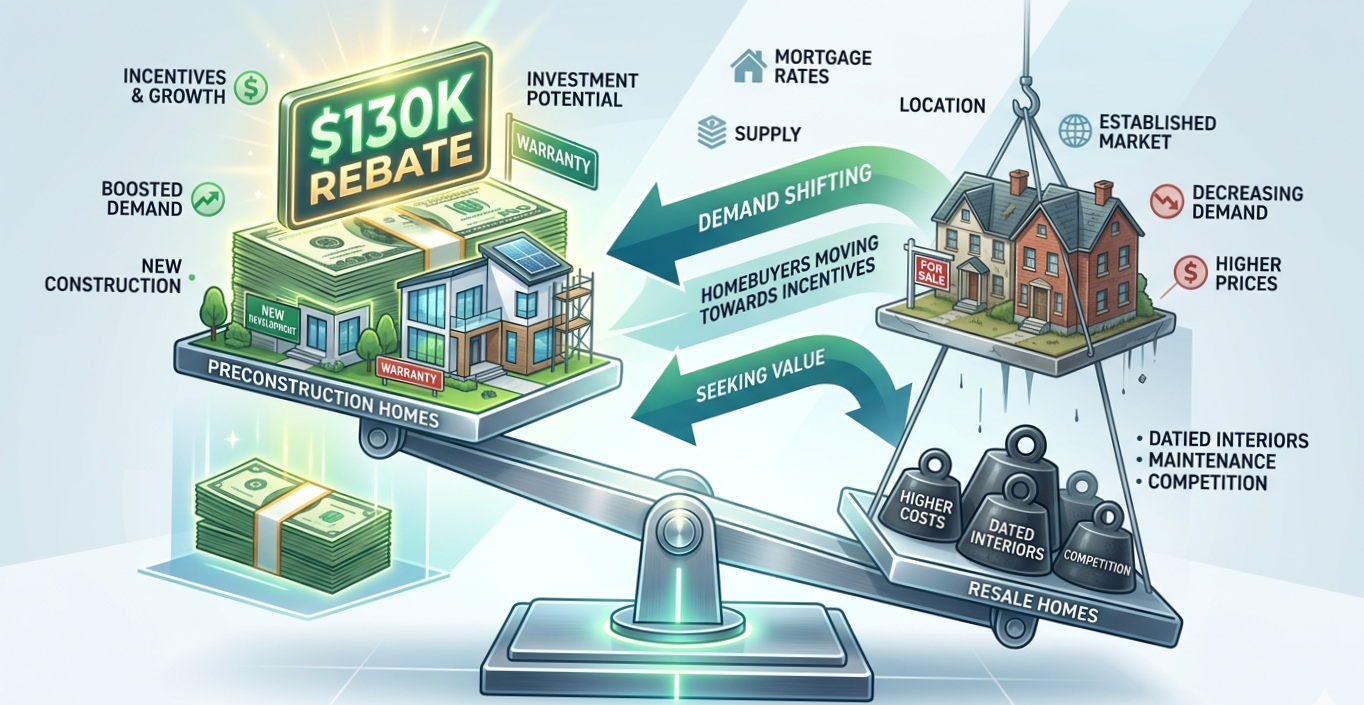

MMM: The $130K “Savings”

Everyone’s celebrating the “up to $130K” HST rebate on preconstruction — but very few people are thinking about what it actually does to pricing.

Here’s the reality.

What I’m Already Seeing

I’ve been speaking with a few realtors who specialize in preconstruction… and developers are already trying to figure out how much more they can charge.

On paper, buyers “save” up to $130K.

In reality?

This resets how pricing works across the entire market.

The Math No One Is Talking About

Let’s simplify this.

Before the rebate:

Preconstruction: $1,000,000

Resale: ~$980,000

Buyers were okay paying a small premium for:

A new build

Delayed closing

Potential appreciation

Now?

That same $1M preconstruction property feels closer to ~$870K after the rebate.

So ask yourself:

Why would anyone pay $980K for resale anymore?

They wouldn’t.

What Happens Next

One of two things plays out.

1. Developers Raise Prices

Developers close the gap and capture the rebate.

Projects that didn’t make sense before suddenly become viable — which could mean:

More supply

More activity

More launches

But there’s a catch.

You’re now locking in today’s price based on future assumptions, in a market where resale demand may weaken.

Appraisal risk becomes real.

2. Resale Prices Adjust Downward

Demand shifts toward preconstruction → resale weakens → comparable sales drop.

This becomes a government stimulus that indirectly puts pressure on existing homeowners… while supporting developers and construction.

The Loop Most People Miss

Here’s how it can play out:

Government subsidizes preconstruction

Developers raise prices

Buyers shift demand

Resale weakens

Comparable sales drop

Preconstruction exit risk increases

It’s a full-circle moment.

There Is an Alternate Outcome

In a perfect world, this rebate creates new demand — not shifted demand.

Preconstruction prices rise

Resale holds steady

Everyone wins

Personally, I don’t think that’s the most likely scenario.

My Take

This policy will absolutely help some buyers and stimulate new construction.

But it will also:

Distort pricing

Shift demand away from resale

Reintroduce real risk into preconstruction investing

I’m not going to tell you what to do.

Just understand the game you’re playing.

Because in markets like this…

Getting it right can make you money

Getting it wrong can cost you six figures

MMM: We Walked Away From a “Good Deal” - Here’s Why

We almost upsized our primary residence recently.

Not a traditional upsize — the home would’ve been roughly the same size, but in an area we actually want to live in long term. On paper, the deal made sense.

The purchase price was about 15% below recent resale comps

It was a new build, so no major renovation risk

It included an ADU, which would’ve brought our net housing cost under $4K/month

It was affordable and manageable on one income

So why didn’t we pull the trigger?

It Wasn’t About Affordability — It Was About Optionality

The numbers worked. But the decision wasn’t purely financial.

Here’s what held us back:

We want to build liquidity right now

The house didn’t check every long-term box

There was no obvious value lift

We’d be parking a large amount of capital in a property we might not even live in

Buying would “peg” us into the market — and transaction costs in real estate are high

That’s when it clicked…

The Market Isn’t Slow Because Buyers Can’t Buy

It’s slow because buyers don’t have to.

This is what a real buyer’s market looks like.

It doesn’t always mean prices are crashing.

It means buyers finally have the luxury of saying no.

And when enough people start saying no…

The market stalls — even if prices haven’t dropped much.

What This Means for Buyers

You have leverage. Use it.

Don’t just ask:

“Can I afford this?”

Start asking:

“Is this the best use of my capital right now?”

That shift in thinking changes everything.

What This Means for Sellers

You’re no longer just competing on price.

You’re competing against patience.

Buyers today are more selective. They’re weighing opportunity cost, liquidity, and flexibility — not just monthly payments.

The Bottom Line

Sometimes the right move isn’t buying.

Sometimes it’s waiting strategically.

If you’re thinking about buying — or sitting on the fence — it’s worth stepping back and evaluating your options carefully. The best decision isn’t always the fastest one.

And in this market, patience can be a powerful strategy.

MMM: War, Oil, and Mortgage Rates What Happens Next?

Whenever a major geopolitical event happens—like rising tensions or conflict involving Iran—one question almost always comes up:

“What does this mean for mortgage rates?”

It’s a great question, and the answer isn’t as straightforward as people expect. In fact, war tends to create two completely opposite forces on interest rates at the same time:

One force pushes rates down

The other pushes rates up

Understanding how these forces interact can help you make smarter decisions when planning a mortgage, refinancing, or home purchase.

Let’s break it down.

1. War Often Slows the Economy (Which Pushes Rates Down)

When geopolitical conflict escalates, uncertainty spreads quickly through the global economy.

Businesses become more cautious. Consumers pull back spending. International trade slows.

This often leads to:

Businesses delaying investments

Consumers reducing spending

Slower global trade and economic activity

When economic growth weakens, central banks typically respond by lowering interest rates to stimulate the economy.

Lower rates encourage:

Borrowing

Business investment

Consumer spending

So from an economic growth perspective, war actually increases pressure for central banks—like the Bank of Canada—to cut interest rates.

2. But War Can Also Create Inflation (Which Pushes Rates Up)

At the same time, geopolitical conflict can disrupt energy supplies and global shipping routes.

Iran is particularly important in global energy markets because it sits near the Strait of Hormuz, one of the most critical oil shipping lanes in the world.

Approximately 20% of global oil shipments pass through this corridor.

If supply in this region becomes disrupted, several things can happen quickly:

Oil prices rise

Gas prices increase

Shipping costs jump

These cost increases push inflation higher globally.

We saw a similar situation during the Russia-Ukraine War, when energy and food prices surged due to supply chain disruptions.

When inflation rises, central banks become less likely to cut interest rates quickly, because lowering rates can fuel even more inflation.

So now we have two competing forces:

Economic slowdown pushing rates down

Inflation pressure pushing rates up

Financial markets are constantly trying to determine which force will dominate.

The Three Phases Markets Go Through After Geopolitical Shocks

Bond markets usually move through three distinct phases when geopolitical conflict begins.

Phase 1: Panic (Investors Buy Bonds)

When uncertainty spikes, investors rush toward safe assets like government bonds.

This surge in demand causes:

Bond demand to spike

Bond yields to fall quickly

For example, during the initial shock, the Government of Canada 5-year bond yield dropped to roughly 2.6% as investors moved capital into safer investments.

Since fixed mortgage rates are closely tied to government bond yields, this can temporarily push mortgage rates lower.

Phase 2: The Real Assessment

Once the initial panic fades, markets begin asking deeper questions.

Investors start evaluating:

What will happen to oil prices?

Will inflation increase?

How long might the conflict last?

If oil prices rise significantly, inflation expectations increase. Investors then demand higher bond yields to compensate for inflation risk.

That’s why bond yields later rebounded to roughly 2.9%.

Phase 3: Repricing Central Bank Policy

In the final phase, markets begin to adjust expectations for central bank policy.

Investors try to predict:

Will the Bank of Canada still cut interest rates?

Will inflation remain elevated?

Could the conflict last longer than expected?

Bond yields adjust based on those expectations.

Because fixed mortgage rates are influenced by bond yields, these market shifts can directly impact mortgage pricing.

What This Means for Real Estate

For real estate and mortgages, the key variable to watch right now is oil.

If oil prices remain elevated:

Inflation could stay stubbornly high

Rate cuts could be delayed

Fixed mortgage rates may remain elevated

But if oil stabilizes and economic slowdown becomes the dominant force:

Bond yields could decline

Fixed mortgage rates may begin to move lower

There are also several domestic factors putting pressure on the Canadian economy right now:

A weakening economy

A softening labour market

Slowing population growth

Because of this, the bigger risk currently appears to be slower rate cuts—not a return to rate hikes.

Markets currently show a very high probability that the Bank of Canada holds rates steady over the next few meetings.

Why Global Events Matter for Your Mortgage Strategy

Mortgage rates don’t just move based on local housing trends. They’re heavily influenced by global economic conditions, inflation expectations, and bond markets.

Understanding how these forces interact can help homeowners and buyers make smarter timing decisions when it comes to:

Mortgage renewals

Refinancing

Purchasing a property

Even small changes in mortgage rates can translate into thousands of dollars in long-term interest costs.

Final Thoughts

Geopolitical events create complex ripple effects across financial markets. While uncertainty can cause short-term volatility in bond yields and mortgage rates, the long-term direction often depends on how inflation and economic growth evolve.

For now, the biggest story in Canada’s mortgage market is likely how quickly—or slowly—rate cuts arrive.

And as global events unfold, those expectations can change quickly.

Know someone renewing their mortgage this year?

Sharing insights like this can help them understand how global events influence mortgage rates—and potentially save them thousands when timing their next move.

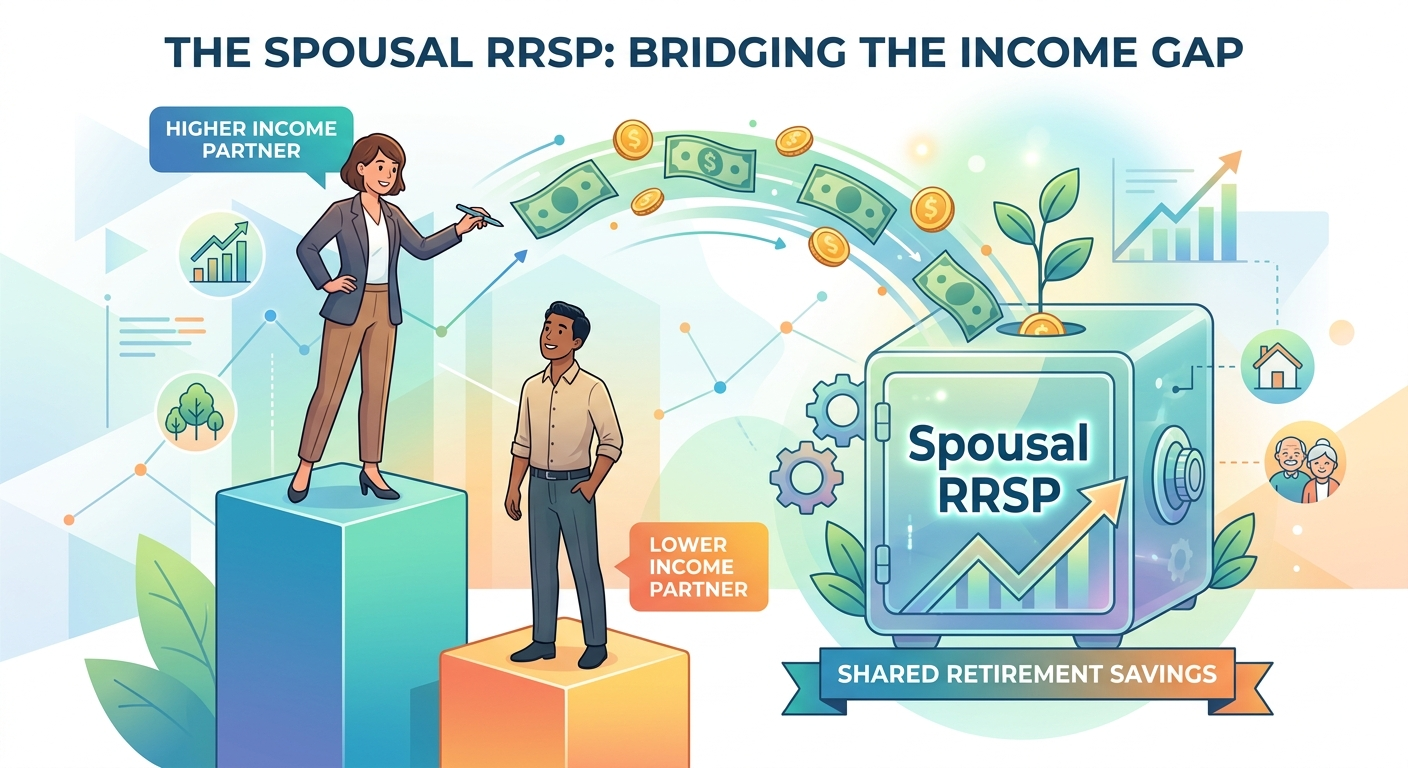

MMM: If There’s an Income Gap in Your Household, Read This.

If one spouse earns significantly more than the other, congratulations — you may have a tax planning opportunity hiding in plain sight.

Recently, I helped a client implement a Spousal RRSP strategy, and it’s one of those moves that’s simple, completely legal, and surprisingly underused.

Alongside mortgages and investing, we also support corporate and select personal tax planning for business owners and incorporated professionals. While reviewing options with this client, the Spousal RRSP made perfect sense and it’s something more families should understand.

Let’s break it down.

What Is a Spousal RRSP?

In simple terms:

One spouse contributes

The other spouse owns the account

The contributor gets the tax deduction

The account holder reports withdrawals later

The purpose?

To shift income from a higher tax bracket today to a lower tax bracket later.

When Does This Strategy Work Best?

A Spousal RRSP is especially powerful when:

One spouse earns $150,000+

The other spouse earns little or significantly less

Future retirement income is expected to be uneven

In many cases, you’re effectively moving income from a ~43%+ marginal tax bracket into a 0–25% bracket later.

That spread matters.

Real Example

Let’s look at a simple scenario:

Spouse A earns: $180,000

Spouse B earns: $0

Spouse A contributes $20,000 to a Spousal RRSP.

Immediate Result

Marginal tax rate: ~41–43%

Estimated tax refund: $8,200–$8,600

That’s real money back today.

Three Years Later

Spouse B withdraws the $20,000.

She has no other income.

Estimated tax payable: ~$1,000–$2,000

The Spread

Tax saved upfront: ~ $8,500

Tax paid later: ~ $1,500

Net household gain: roughly $6,000–$7,000.

That’s not an investment return — that’s purely tax arbitrage.

Important: The Attribution Rule

There’s one key rule you must respect.

If the lower-income spouse withdraws funds:

In the same year of contribution, or

Within the next two calendar years,

The income may be attributed back to the contributing spouse.

Simply put:

If you contribute and withdraw too soon, the strategy collapses.

Practically speaking — wait three calendar years before withdrawing.

A Limited but Powerful Application

Here’s where most people miss the opportunity:

If a spouse is going on parental leave and will temporarily fall into a very low tax bracket — that can be a strategic time to withdraw.

Other strong use cases:

Stay-at-home partners

A self-employed spouse who can draw income strategically

Couples expecting uneven retirement income

In those cases, you may want to consider maximizing the lower-income spouse’s position first.

Final Thought

A Spousal RRSP isn’t for everyone. But when there’s a meaningful income gap between spouses, it can create thousands of dollars in tax savings — legally and efficiently.

Sometimes the best strategies aren’t complicated.

They’re just underutilized.

MMM: Positive Cash Flow Isn’t the Win You Think It Is

There’s a pattern I see all the time.

Someone owns two or three investment properties.

Their net worth is north of $1M.

They’re cash-flow positive.

But they aren’t really growing.

Most portfolios I review aren’t failing.

They’re just quietly underperforming.

And the toughest part?

It feels good.

Very few investments make you feel more successful while your actual return declines.

“I’m Busy. I Own Assets. Why Don’t I Feel Richer?”

Here’s a common example — especially with buyers from 2015–2017.

After about 10 years of ownership, this is what I often see:

Property value: $1,200,000

Mortgage balance: $400,000

Equity: $800,000

Cash flow: $1,000/month ($12,000/year)

Rents have increased.

Mortgage balances have dropped.

Payments stayed roughly the same.

On the surface, this looks great.

But let’s calculate the real return.

The Real Return on Equity

Annual cash flow: $12,000

Mortgage paydown (~3%): ~$12,000

Total annual return: $24,000

Now divide that by $800,000 in equity:

$24,000 ÷ $800,000 = 3% Return on Equity (ROE)

You’re sitting on $800,000…

And earning roughly GIC-level returns.

That’s the trap.

Returns decay.

Capital gets stuck.

Growth slows — even though it doesn’t feel like it.

The Hidden Tax Trap No One Talks About

It gets worse.

As mortgages shrink → taxable income rises.

As taxable income rises → marginal tax rates climb.

If you own personally:

Bracket creep slowly erodes returns.

If you own in a corporation:

Passive income can be taxed at roughly 50%.

The CRA and the people of Canada thank you for your contribution.

Meanwhile, your equity keeps compounding… slowly.

How to Know If You’re Stuck

Here’s a quick self-test:

Your ROE is below 4–5%

Equity represents more than 60% of the property value

There’s no meaningful value-add opportunity left

If you hit two or three of these, your portfolio may not be working hard enough.

What I Do Differently

Everything is always for sale.

I have zero emotional attachment to individual assets.

If a property no longer makes financial sense, it can go.

“I shouldn’t sell — the market is down.”

“I could’ve made more at the peak.”

Those thoughts don’t drive my decisions.

Only two questions matter:

What is my return on equity relative to my risk?

Is there any meaningful value-add left?

If the answer isn’t compelling, capital gets redeployed.

The Real Rule

Cash flow keeps you alive.

ROE tells you if you’re growing.

Strategy determines whether you win.

Final Thought

If this doesn’t apply to you yet, bookmark this.

One day, it will.

If you’ve owned properties for 10+ years, it may be time for a financial health check.

MMM: Why Paying Down Your Rental Mortgage Faster Isn’t Always the Smartest Move

If you’ve owned rental properties for a while and have been aggressively paying down the mortgage, first off — that’s a good thing.

You’ve likely:

Lowered your risk

Built meaningful equity

Felt responsible and disciplined

And you should feel good about that.

But if you still have 15–20 years left on your rental mortgage, I want to challenge how you’re thinking about this strategy.

Because while paying down debt feels right, it doesn’t always put you in the strongest position today.

The Reality Most Investors Miss

Paying down your rental mortgage faster feels productive.

But what actually matters more in the current environment is:

Liquidity

Tax optimization

Cash flow

Flexibility

And there’s a simple move many long-term rental owners overlook.

Re‑Amortizing Your Mortgage

If you’ve been paying down your rental for 8–10 years (or more), there’s a strong chance you can re‑amortize the remaining balance.

What does that mean?

You spread the same remaining mortgage balance over a longer period again.

No new debt. No refinancing games. Just resetting the amortization.

In many cases, this can:

Reduce your monthly payment by ~20% or more

Instantly improve cash flow

Why This Matters More Than You Think

Lower monthly payments do more than just feel comfortable.

They:

Create a cash buffer

Absorb bad months

Help cover vacancies and repairs

Protect you from rate changes

Reduce the chance of being forced into a bad decision

Paying down debt improves optics.

Cash flow gives you options.

And options give you control.

Control is what keeps you in the game long term.

The Bigger Picture

If you’re early in your mortgage journey, aggressively paying down debt can make sense.

But if you’re halfway through — or still have decades left — it’s worth asking yourself:

Would I rather feel responsible… or actually be more resilient?

The strongest investors aren’t just disciplined.

They’re flexible.