MMM: Rates moved Most people missed it.

Over the past few weeks, I’ve been having the same conversation again and again:

“Should I take my lender’s renewal offer… or wait?”

If that’s something you’ve been wondering too, you’re not alone.

And if you’re still holding a rate from early March that hasn’t expired yet —

you may want to seriously consider taking it.

Let’s break down why.

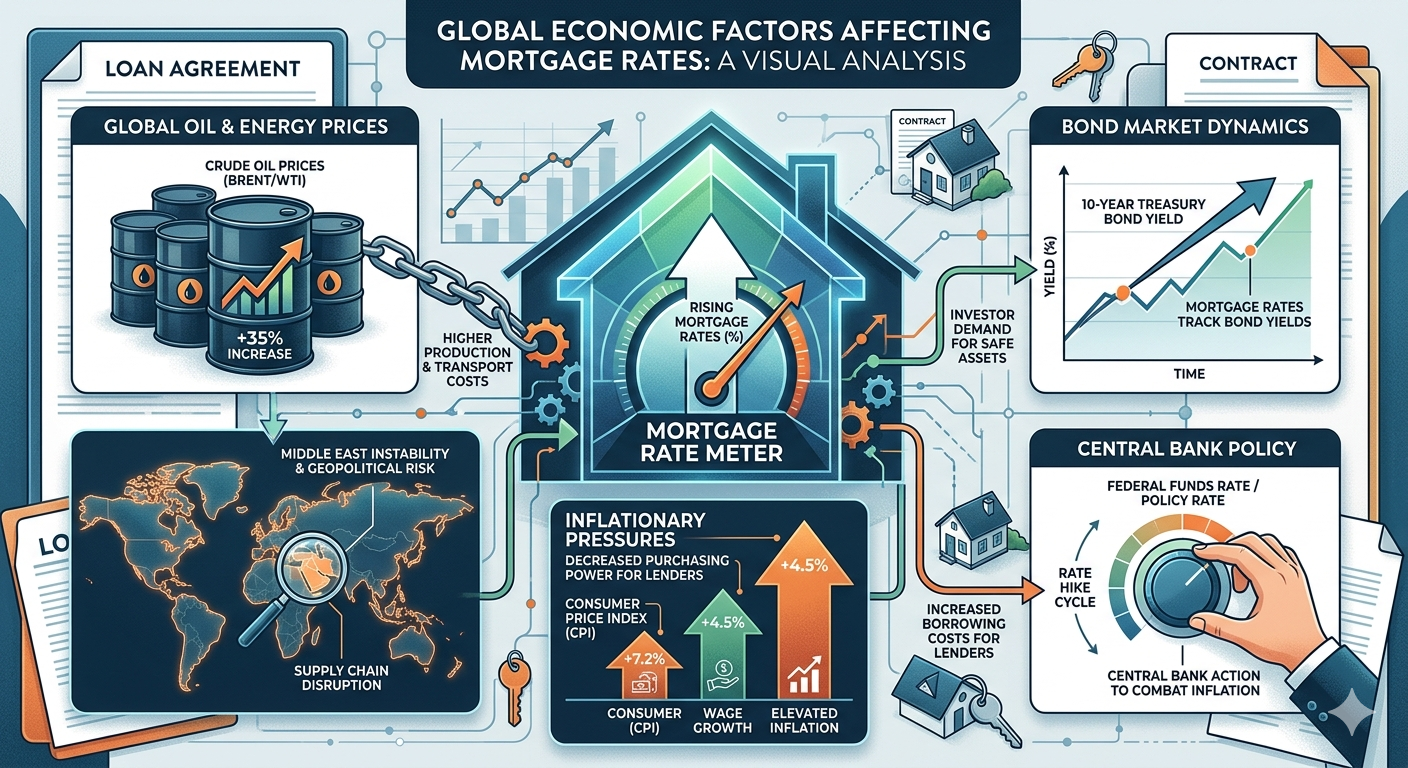

Rates Have Already Moved

Fixed mortgage rates are closely tied to the Canada 5-year bond yield — and recently, that’s been on the rise.

Over just a few weeks:

The Canada 5-year bond yield jumped to around 3.08%

That’s an increase of about 0.45%

At one point, it even spiked close to 0.65%

When bond yields rise, fixed mortgage rates follow — often quickly.

What Caused the Shift?

Here’s the short version of what’s been happening globally:

Ongoing Middle East conflict pushed oil prices higher

Rising oil prices increased inflation risk

Higher inflation expectations caused bond yields to jump

Even the Bank of Canada has acknowledged:

More uncertainty

Higher inflation risk

Slower economic growth

Where People Get It Wrong

This is something I see every cycle:

When things feel calm → people lean toward variable rates

When things feel uncertain → people rush into fixed rates

The problem?

By the time it feels risky…

👉 Fixed rates have already gone up

👉 And you’re locking in too late

The best time to consider fixed rates is usually when no one is talking about them — not when everyone is reacting.

The Bottom Line

If your mortgage is renewing in the next 3 to 6 months, here’s what matters most:

Don’t overthink trying to “time” interest rates

Don’t ignore a solid offer that’s already in front of you

Focus on strategies that have a bigger impact, like:

Debt consolidation

Re-amortization

Setting up a HELOC