MMM: The Fixed vs Variable Question Everyone Is Asking

The Bank of Canada is announcing its latest interest rate decision this week, and while no major changes are expected, one question continues to come up:

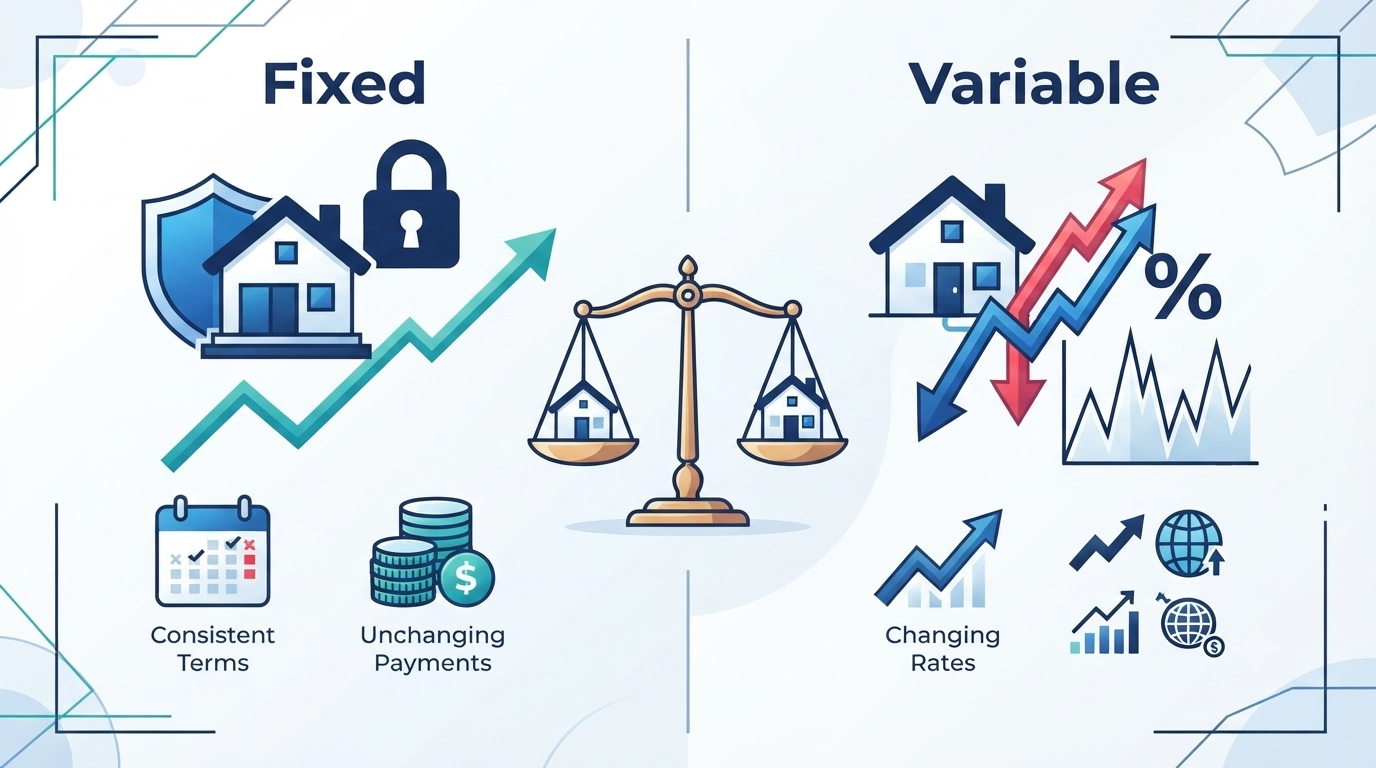

Should I choose a fixed or variable mortgage?

Many people make this decision by comparing today's mortgage rates. If variable rates are lower, it might seem like the obvious choice. If fixed rates are lower, the opposite may feel true.

But the reality is more nuanced.

It's Not Just About Today's Rate

Instead of asking:

"Which mortgage has the lower interest rate today?"

Consider asking:

"Who do I want to carry the risk?"

This simple shift in perspective can help you make a more informed financial decision.

Understanding Variable Mortgages

With a variable-rate mortgage, you're taking on the interest rate risk yourself.

If interest rates decrease, your mortgage could become more affordable.

If rates increase, your borrowing costs may rise.

The potential for savings comes with the possibility of higher costs if market conditions change.

Understanding Fixed Mortgages

A fixed-rate mortgage works differently.

When lenders determine a fixed mortgage rate, they don't simply choose a number. They look closely at the Government of Canada bond market, particularly the five-year bond yield.

That market already reflects expectations about:

Future Bank of Canada rate changes

Inflation

Economic growth

Investor expectations over the coming years

Lenders then add their costs and profit margin before offering you a fixed rate.

In other words, choosing a fixed mortgage means you're paying for predictability and stability.

Neither Option Is Automatically Better

It's common to hear people ask whether fixed or variable is the "better" mortgage.

The truth is that both options are priced based on today's market expectations.

A higher fixed rate doesn't necessarily mean it's a worse deal, and a lower variable rate doesn't automatically make it the smarter choice.

The key difference is who absorbs the uncertainty if the future doesn't unfold as expected.

Variable: You take on the risk.

Fixed: The lender takes on more of that risk, and you pay for the certainty.

Which Option Is Right for You?

Rather than focusing only on today's interest rates, think about your own comfort level with uncertainty.

Ask yourself:

Which type of risk am I more comfortable managing?

For some homeowners, the flexibility of a variable mortgage makes sense. For others, the stability of fixed payments provides valuable peace of mind.

The best mortgage isn't always the one with the lowest rate—it's the one that aligns with your financial goals, your budget, and your tolerance for risk.

If you're deciding between fixed and variable, take the time to look beyond the numbers. Understanding the trade-offs can help you make a decision that works for you both today and in the years ahead.