MMM: If There’s an Income Gap in Your Household, Read This.

If one spouse earns significantly more than the other, congratulations — you may have a tax planning opportunity hiding in plain sight.

Recently, I helped a client implement a Spousal RRSP strategy, and it’s one of those moves that’s simple, completely legal, and surprisingly underused.

Alongside mortgages and investing, we also support corporate and select personal tax planning for business owners and incorporated professionals. While reviewing options with this client, the Spousal RRSP made perfect sense and it’s something more families should understand.

Let’s break it down.

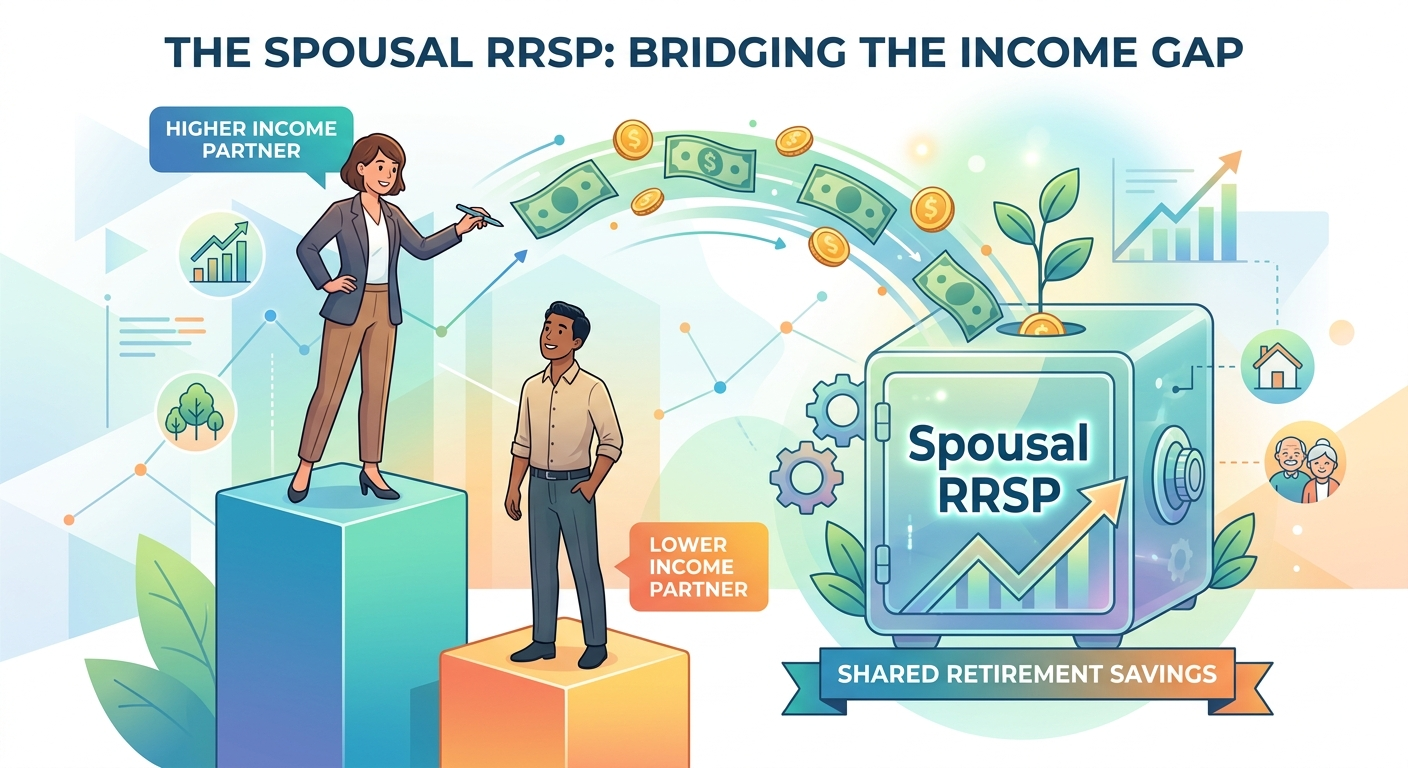

What Is a Spousal RRSP?

In simple terms:

One spouse contributes

The other spouse owns the account

The contributor gets the tax deduction

The account holder reports withdrawals later

The purpose?

To shift income from a higher tax bracket today to a lower tax bracket later.

When Does This Strategy Work Best?

A Spousal RRSP is especially powerful when:

One spouse earns $150,000+

The other spouse earns little or significantly less

Future retirement income is expected to be uneven

In many cases, you’re effectively moving income from a ~43%+ marginal tax bracket into a 0–25% bracket later.

That spread matters.

Real Example

Let’s look at a simple scenario:

Spouse A earns: $180,000

Spouse B earns: $0

Spouse A contributes $20,000 to a Spousal RRSP.

Immediate Result

Marginal tax rate: ~41–43%

Estimated tax refund: $8,200–$8,600

That’s real money back today.

Three Years Later

Spouse B withdraws the $20,000.

She has no other income.

Estimated tax payable: ~$1,000–$2,000

The Spread

Tax saved upfront: ~ $8,500

Tax paid later: ~ $1,500

Net household gain: roughly $6,000–$7,000.

That’s not an investment return — that’s purely tax arbitrage.

Important: The Attribution Rule

There’s one key rule you must respect.

If the lower-income spouse withdraws funds:

In the same year of contribution, or

Within the next two calendar years,

The income may be attributed back to the contributing spouse.

Simply put:

If you contribute and withdraw too soon, the strategy collapses.

Practically speaking — wait three calendar years before withdrawing.

A Limited but Powerful Application

Here’s where most people miss the opportunity:

If a spouse is going on parental leave and will temporarily fall into a very low tax bracket — that can be a strategic time to withdraw.

Other strong use cases:

Stay-at-home partners

A self-employed spouse who can draw income strategically

Couples expecting uneven retirement income

In those cases, you may want to consider maximizing the lower-income spouse’s position first.

Final Thought

A Spousal RRSP isn’t for everyone. But when there’s a meaningful income gap between spouses, it can create thousands of dollars in tax savings — legally and efficiently.

Sometimes the best strategies aren’t complicated.

They’re just underutilized.